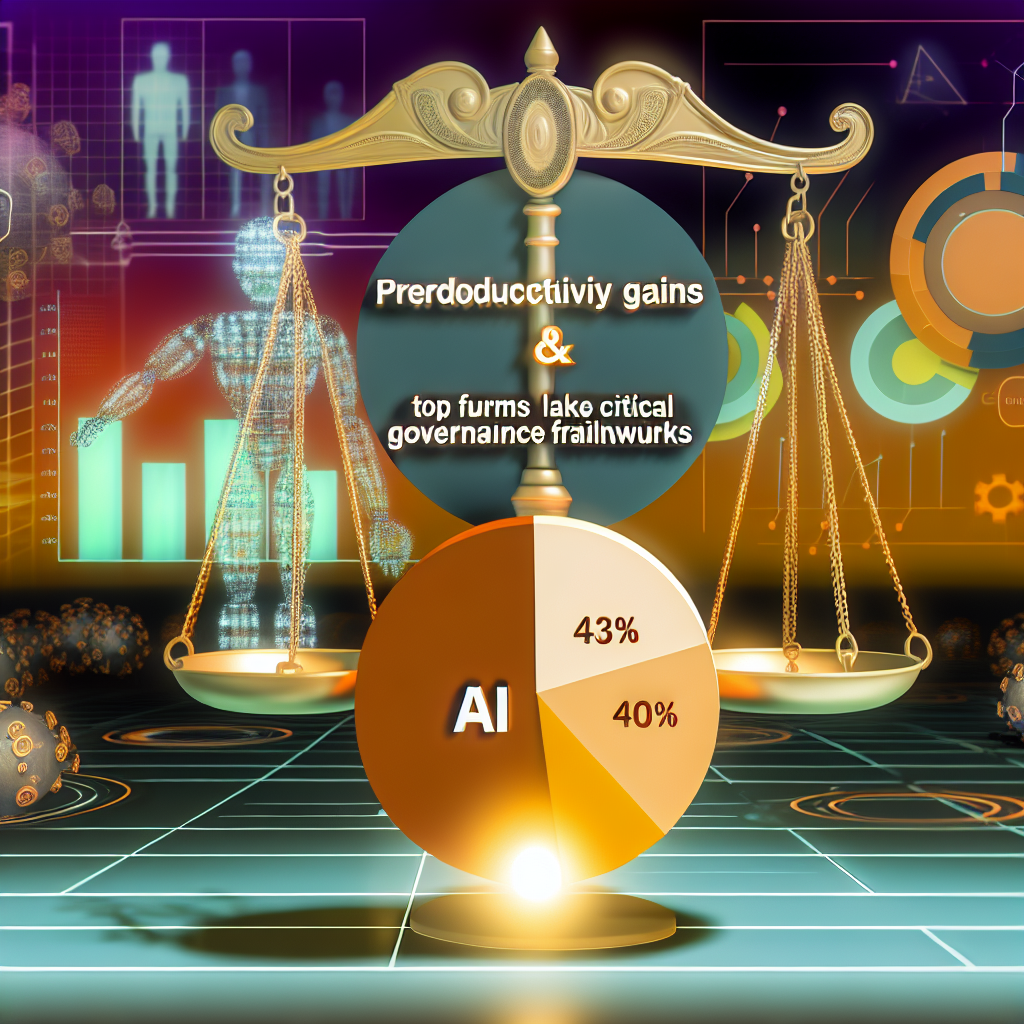

15 min read 0 AI Business Balancing Productivity Gains and AI Risk: Why 43% of Top Firms Lack Critical Governance Frameworks Rosario Fortugno April 5, 2026

10 min read 0 Artificial Intelligence Business Project Management SpaceX’s xAI Acquisition: Pioneering Orbiting AI Data Centers and the Future of Space-Based Compute Rosario Fortugno April 3, 2026

15 min read 0 Business Project Management Tesla’s Terafab Project Accelerates with Technical Program Manager Recruitment Rosario Fortugno March 24, 2026

15 min read 0 Business Elon Musk EVs Elon Musk’s Terafab: A Record-Breaking Chip-Building Vision for American Manufacturing Rosario Fortugno March 22, 2026

1 min read 0 AI Business OpenAI launches GPT‑5.4 with Pro and Thinking versions Rosario Fortugno March 16, 2026

13 min read 0 Artificial Intelligence Business Project Management Space Exploration How SpaceX’s Plan for 1 Million Orbiting AI Data Centers Threatens Astronomy and the Space Economy Rosario Fortugno March 14, 2026

15 min read 0 Business Project Management How Billion-Dollar Infrastructure Deals Are Powering the AI Boom: A CEO’s Insider View Rosario Fortugno March 4, 2026

15 min read 0 AI Artificial Intelligence Business Tesla Emerges as a ‘Physical AI’ Powerhouse: Q4 Earnings Beat and $2 Billion xAI Stake Catalyze AI Productivity Leap Rosario Fortugno February 24, 2026

14 min read 0 Business Project Management SpaceX and xAI Merge: Pioneering the Future of Space-Based AI Infrastructure Rosario Fortugno February 22, 2026

14 min read 0 Artificial Intelligence Business Project Management Orbital AI Revolution: Musk’s Vision for AI in Space & SpaceX’s Hyper-Hyper Scaling Rosario Fortugno February 12, 2026